Metalworking Activity Holds Steady in March

Overall metalworking activity leveled off in March, but not to a point of concern.

Metalworking activity remains in contraction, landing in March at the same index as February, following three straight months of slowing contraction. Metalworking has manifested this “stall” followed by “recovery” every few months for the past year, suggesting no cause for concern. March closed at 47.9 compared to February’s 47.7.

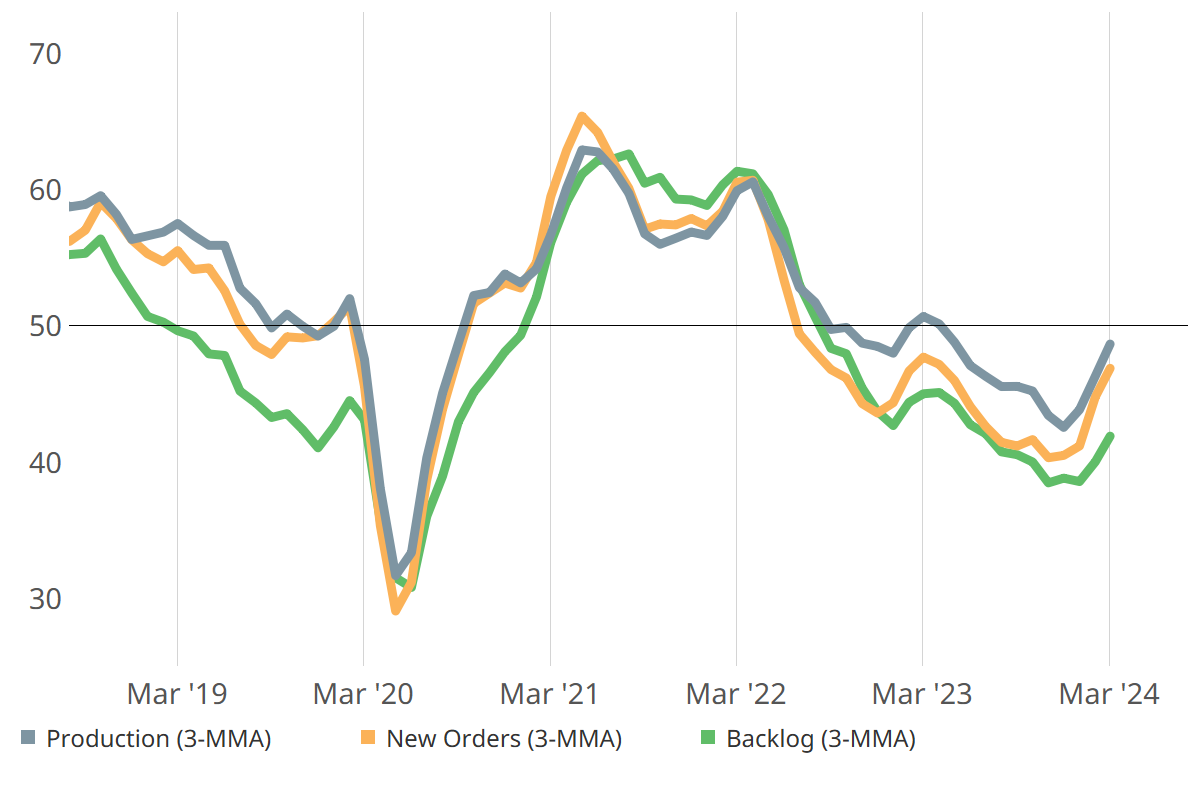

March marked another month of slowing contraction in three key components: new orders, production and backlog. While still contracting, the consistent creep of all three toward 50 is encouraging. Employment and exports contracted again in March at nearly the same rates as February, similar to the overall index activity. Supplier deliveries also maintained a steady rate and consistent position in the expansion half of the graph.

Business expectations for the next 12 months have increased for five months straight, which — despite being just a sentiment — has to mean something good.

The Metalworking GBI stayed steady in March. Source: Gardner Intelligence

Another month of slowed contraction in new orders, production and backlog is associated with a steady overall index in March (3-MMA = three-month moving averages). Source: Gardner Intelligence

Related Content

-

Metalworking Activity Continues its Roller Coaster Year of Contraction

October marks a full year of metalworking activity contracting, barring just one isolated month of reprieve in February.

-

Metalworking Activity is Nearing a Full Year of Contraction

Metalworking activity has contracted since October of 2022.

-

Metalworking Activity Stays Flat in October

The GBI for Metalworking reflects stability of most of the six GBI components that had been losing ground months prior. Ordinarily underwhelming, flat is good when it means not contracting.